Content

- What are the most common accounting issues for prepaid rent?

- Accounting for base rent with journal entries

- Facilitating tax reductions

- Prepaid Expenses: Definition, Examples & Recording Process

- Lease modifications- common accounting issues for prepaid rent

- How organizations can ensure they account for prepaid correctly?

- Why are prepaid expenses an asset?

Prepaid expenses are basically future expenses which have been paid in advance, with common examples being insurance or rent. These expenses are initially documented as an asset on the firm’s balance sheet, and as its benefits are eventually realised over time, they would then be classified as an expense. From a company’s point of view, an increase in prepaid expenses is a debit. Later, when the prepaid expense is used, a company records an expense for the product or service which is a debit, and the prepaid expense gets canceled out through a credit. While prepaid expenses are initially recorded as an asset, they eventually transition to an expense on the income statement when the product or service is incurred.

Is prepaid rent a current asset or current liability?

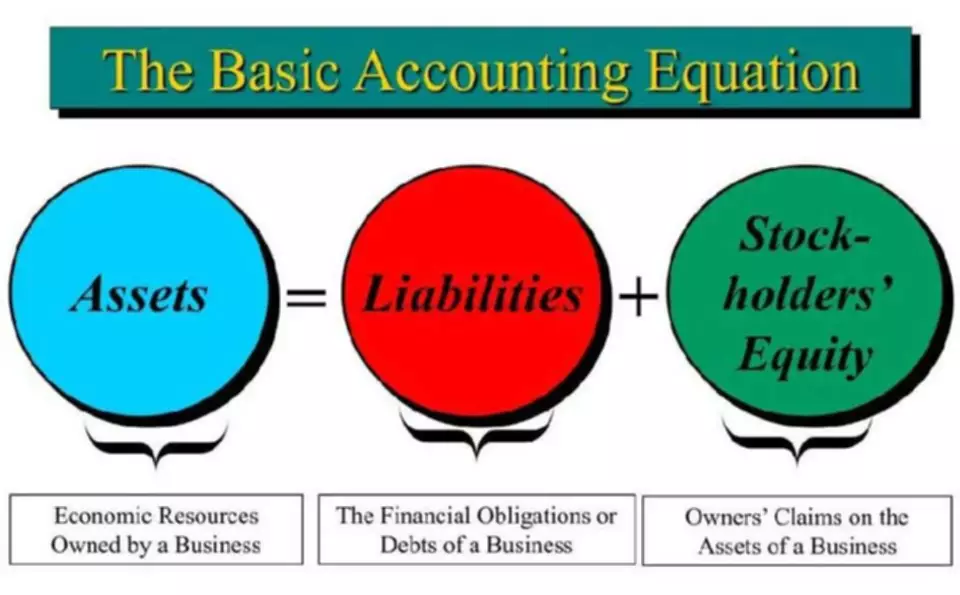

Prepaid expenses—which represent advance payments made by a company for goods and services to be received in the future—are considered current assets. Although they cannot be converted into cash, they are payments already made.

Prepaid expense amortization is the process of gradually decreasing an asset’s value to zero over the time that the prepaid expense adds value to the company. It serves as a method of recording how quickly a prepaid expense was used up. Prepaid expenses are essentially prepayments that have been made for a product or service whose value will only be realised in the future.

What are the most common accounting issues for prepaid rent?

The reason is that a high proportion of assets to liabilities indicates a sign of a higher degree of liquidity. Organizations can ensure they account for prepaid rent correctly by implementing steps and controls and adhering to the accounting principles and standards, such as GAAP or IFRS. This article will explore whether prepaid rent is an asset and provide a detailed analysis of the factors you must consider when answering this question.

Is prepaid rent an asset on the balance sheet?

Prepaid rent is recorded as an asset on the balance sheet and is initially recognized when you pay. As the period covered by the prepaid rent payment occurs, you decrease the prepaid rent asset account and increase the rent expense account.

When a company prepays for an expense, it is recognized as a prepaid asset on the balance sheet, with a simultaneous entry being recorded that reduces the company’s cash (or payment account) by the same amount. Most prepaid expenses appear on the balance sheet as a current asset unless the expense is not to be incurred until after 12 months, which is rare. These kinds of goods or services that are paid for in advance cannot be expensed immediately because the expense would not line up with the benefit incurred over time from using the asset. Prepaid rent, which is our main focus is a type of prepaid expense and as such is an example of a current asset. The prepaid rent is recorded initially as an asset, but its value is expensed over time onto the income statement.

Accounting for base rent with journal entries

The amortisation of prepaid expenses may be particularly difficult for corporations that are still reliant on manual accounting protocols as this creates lots of room for human errors to surface. For instance, if an accountant forgets to document an expense or factor in a prepaid expense that has already been amortised, this may lead to inaccurate financial reporting. Consequently, such mistakes may have a significant impact on the business decisions made as well as the firm’s tax reporting accuracy. Consequently, insurance expenses will need to be prepaid by the enterprise clients. Besides that, another notable example would be if the company purchases a huge and costly printer that it intends to utilise over time, the printer may then be acknowledged as a prepaid expense. In other words, this means that the printer will provide its benefits to the firm across its entire lifetime rather than just when it was just bought.

- By outsourcing, businesses can achieve stronger compliance, gain a deeper level of industry knowledge, and grow without unnecessary costs.

- Prepaid insurance is insurance paid in advance and that has not yet expired on the date of the balance sheet.

- As the name implies, Prepaid Expenses represent a prepayment for a future expense.

- Use of our products and services are governed by our Terms of Use and Privacy Policy.

Prepaid expenses are recognised as a type of asset because they represent products and services whose benefits will only be incurred at a later date. Thankfully though, companies may still drastically lower their risk of encountering minor errors by automating their entire accounting procedure using smart credit control platforms like Kolleno. In summary, Kolleno is an all-in-one software that can be integrated into a business’s existing workflow, with the accounting team being seamlessly onboarded in no time. Thus, the firm need not waste time and human resources to learn a completely novel accounting tool for their day-to-day operations.

Facilitating tax reductions

Therefore, when a company prepays for an expense, it is recognized as an asset on the balance sheet. The amount paid is entered into the prepaid expense account with a simultaneous entry to reduce the company’s cash or payment account by the same amount. Rent is commonly paid in advance, being due on the first day of that month covered by the rent payment. The landlord typically sends an invoice several weeks early, so the tenant issues a check payment at the end of the preceding month in order to mail it to the landlord and have it arrive by the due date.

- The amount recognized as an expense corresponds to the prepayment portion utilized during the specific period.

- It is crucial to remember that these costs are initially not listed on the income statement due to the GAAP matching concept.

- Additional expenses that a company might prepay for include interest and taxes.

- It’s one of the core financial statements for any business, along with your cash flow statement, debtor reports and the profit and loss statement.

Ignite staff efficiency and advance your business to more profitable growth. Transform your order-to-cash cycle and speed up your cash application process by instantly matching and accurately applying customer payments to customer invoices in your ERP. As soon as the corporation uses up the accrual, the expense is transferred to the profit and loss statement for that period. Visual Lease Blogs – read about the best lease administration software, lease management solutions, commercial lease accounting software & IFRS 16 introduction. Not to mention, Kolleno’s software is also designed to remove manual Excel spreadsheet-reliant procedures to automate the entire accounting process for a wide range of companies. Does the Prepaid Rent account flow into the income statement, statement of owner’s equity, or balance sheet?

Prepaid Expenses: Definition, Examples & Recording Process

The cost is not recognized right away because the business has not yet reaped any benefits from the services. The business would record an expense as new invoices came in and deduct the prepaid asset in the same account. A schedule amortization might be used to progressively reduce any prepaid rent or insurance to zero.

The accounts that are reported on the balance sheet such as assets, liabilities, and equity accounts are said to be permanent accounts. They are considered permanent accounts because they continue to maintain ongoing balances over time and are not closed at the end of the accounting period. As the rental period or periods covered by the prepaid rent payment occur, the prepaid rent asset account is decreased, and the rent expense account is increased. At the end of each accounting period, a journal entry is posted for the expense incurred over that period, according to the schedule.

Lease modifications- common accounting issues for prepaid rent

As a result, prepaid expenses are a crucial component of accounting and finance that aids companies in efficiently managing their cash flow expenses. These costs are payments made upfront for goods and services that a business will use or consume in the future. To help businesses stay on track with their prepaid expenses, it would always be a good idea to consider adopting an automated accounting software to ensure that no information slips through the cracks. By doing so, companies can rest assured that their financial reports and statements are consistently accurate and reliable.

Similarly to ASC 840, this straight-line lease expense is calculated as the sum of all of the rent payments over the lease term and divided by the total number of periods. A full example with journal entries of accounting prepaid rent accounting for an operating lease under the new accounting standards can be found here. In a scenario with escalating lease payments, the average expense recorded is more than the lower payments at the beginning of the lease term.

Sometimes, businesses prepay expenses because they can receive a discount for prepayment. Prepaid expenses may also provide a benefit to a business by relieving the obligation of payment for future accounting periods. There may also be tax benefits concerning prepaid expenses, however, all organizations must follow the proper rules related to tax deductions. Prepaid expenses are a crucial factor in determining a company’s short-term financial stability because they are a current asset. When the benefits of prepaid expenses are realized, they are recorded as an expense on the income statement.

- Therefore, prepaid rent is first recorded on the balance sheet, in the prepaid expense/asset account because it represents a future benefit that is due to the business.

- The asset’s value gradually declines as the advantages of the deferred expense are realized over time, and a corresponding sum is expensed on the income statement.

- As the benefits of the prepaid expense are realized, it is recognized on the income statement.

- Having a legal retainer is usually a necessity before a law firm, or an attorney can kickstart the representation.

- Your success is our success.From onboarding to financial operations excellence, our customer success management team helps you unlock measurable value.

Every month, the journal entry further decreases the prepaid expense account balance as the value of the coverage period is recognized by the business. The initial journal entry for a prepaid expense has no impact on the financial accounts of a corporation. For example, repaid rent is debited and cash is credited in the first journal entry for prepaid rent. Both of these accounts are considered assets, so they do not affect a company’s balance sheet.

Recent Comments